Don’t let a (tax) savings opportunity pass you by – there is still time to add cash to your self-directed IRA and take advantage of the related tax breaks for 2022. The tax rules generally allow IRA owners to contribute to their IRAs up until their tax-filing deadline for the year, but tax rules tend to not be that simple. Here is a breakdown of the dates and contribution rules for 2022 contributions to keep you on track.

1. DETERMINE YOUR DEADLINE TO CONTRIBUTE TO AN IRA

You can deposit an IRA contribution for tax year 2022 from January 1, 2022, through your federal income tax-filing due date for 2022. If your personal tax year follows the calendar year, your federal income tax-filing deadline is April 15, 2023, which falls on a Saturday. When that happens, taxpayers may file their taxes (and make IRA contributions) on the next business day. But the next business day, April 17, 2023, is Emancipation Day, a holiday observed in Washington D.C. Because this is considered a legal holiday, the tax-filing and IRA contribution deadline is bumped to the next business day: Tuesday, April 18, 2023. Residents of Maine and Massachusetts have until April 19, 2023, to file tax returns and make IRA contributions because these two states observe Patriots’ Day on April 18. Although you may apply for an extension to delay filing your 2022 income tax return until October 16, 2023, IRA contributions must be made by your applicable April deadline.

The IRS may extend your tax-filing deadline if you live in a federally declared disaster area. As of March 1, 2023, taxpayers in most of California and parts of Alabama and Georgia have until October 16, 2023, to file federal tax returns and make IRA contributions because FEMA declared disaster areas in those states following severe weather events.

2. DECIDE IF YOU WANT TO CONTRIBUTE TO A TRADITIONAL IRA, ROTH IRA, OR BOTH

If you’re eligible to contribute to both a Traditional IRA and Roth IRA, you may contribute to both in the same year. Oftentimes, IRA owners choose a Traditional IRA because the tax deduction for a contribution lowers their taxable income (and potentially their tax liability) for the year. A Roth IRA, on the other hand, may be attractive if you think your tax rates will be higher by the time you need to withdraw money from your IRA, you need access to your IRA savings before you reach age 59½, or you want to take tax-free distributions in retirement.

Am I eligible to make a 2022 Traditional IRA contribution?

Am I eligible to make a 2022 Traditional IRA contribution?

Anyone with earned income can make a Traditional IRA contribution. Your contribution will be fully deductible unless you or your spouse are covered by an employer’s retirement plan, such as a 401(k) plan. If you or your spouse are participating in a workplace retirement plan, your ability to take a tax deduction for your Traditional IRA contributions depends on your modified adjusted gross income (MAGI).

- If you are married, filing a joint tax return, and participated in a retirement plan in 2022, your annual IRA contribution will be fully deductible if your MAGI is $116,000 or less. Your contribution will be partially deductible if your MAGI is between $116,000 and $136,000. If your MAGI is $136,000 or higher, your Traditional IRA contribution will not be deductible.

- If you didn’t participate in an employer’s plan in 2022 but your spouse did, your MAGI must be $218,000 or less to take a full deduction. No deduction is available if your MAGI is $228,000 or more.

- If you are single and participating in an employer’s retirement plan, your deduction is phased out with MAGI between $73,000–$83,000.

If you don’t qualify to take a tax deduction, you may still contribute to a Traditional IRA. You may file Form 8606 with your tax return to track the nondeductible contributions in your IRA, so you won’t have to pay tax on those dollars again when you take money out of your IRA in the future.

Am I eligible to make a 2022 Roth IRA Contribution?

Am I eligible to make a 2022 Roth IRA Contribution?

You may contribute to a Roth IRA only if you have earned income that falls below certain limits.

- If you are married and filing a joint tax return for 2022, you may make the maximum contribution to a Roth IRA if your MAGI is $218,000 or less. If your MAGI is between $218,000 and $228,000, you may make a partial contribution. If your MAGI is $228,000 or higher, you cannot contribute to a Roth IRA for 2022.

- If you are single, the amount you are eligible to contribute to a Roth IRA is phased out with MAGI between $138,000–$153,000.

3. MAKE SURE YOU DON’T CONTRIBUTE TOO MUCH

If you’re eligible to make a full contribution for 2022, you can deposit a maximum of $6,500 between your Traditional and Roth IRAs. If you’re age 50 or older, you can contribute an extra $1,000 – for a total of $7,500 – between your Traditional and Roth IRAs.

A married couple filing a joint tax return can each make the maximum contribution if each is eligible and has an IRA. Together, spouses could contribute $13,000 ($15,000 if both are over age 50) for the 2022 tax year.

If you have put too much in your IRA, don’t worry – you have multiple options for correcting an excess.

4. NOTIFY YOUR CUSTODIAN WHEN MAKING A CONTRIBUTION FOR THE PRIOR YEAR

If you make your 2022 IRA contribution in 2023, you must inform your IRA custodian when you make your contribution that it is for tax year 2022. Without this instruction, IRA custodians will record it as a current-year contribution. This may cause problems for you if your tax return indicates a 2022 IRA contribution was made, but it is not reported by your IRA custodian. Accurately reporting a contribution for the prior tax year by your IRA custodian will also ensure that you do not inadvertently use up your 2023 contribution limit.

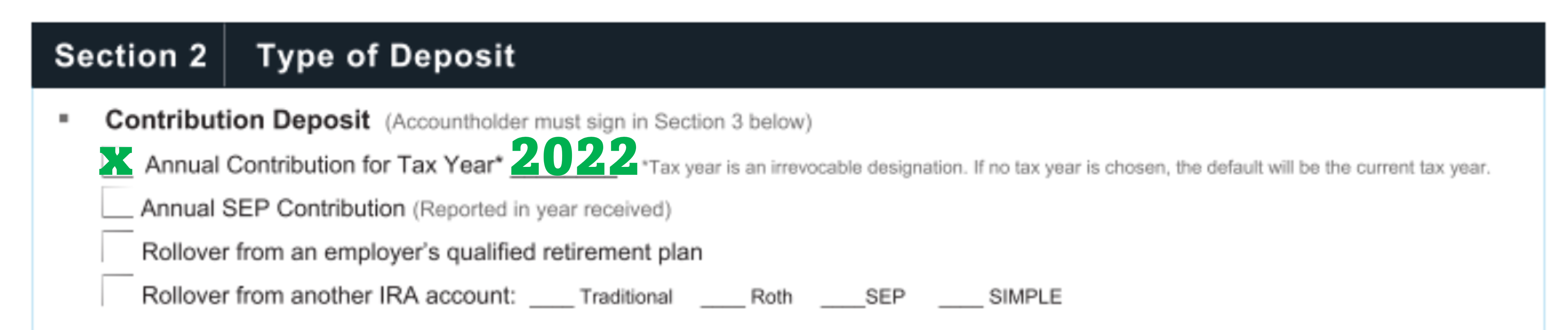

For STRATA account holders, you can make an annual contribution for tax year 2022 by filling out the Deposit Certification Form and filling in Section 2 for the 2022 tax year. Payment instructions can be found on the form and in our FAQs.

Additional Resources

Disaster-Related Extensions

- The current list of eligible localities and other details for each disaster are available on the Tax Relief in Disaster Situations page on IRS.gov.

Helpful Forms for 2022

- IRS Form 8606 and Instructions – File this form with your federal income tax return to track nondeductible contributions in your Traditional IRA.

- STRATA Deposit Certification Form – Make a one-time contribution to your STRATA IRA by submitting this form prior to sending your funds. (Funding and submission instructions are provided on the form.)

Learn More About 2022 and 2023 Contribution Limits

- IRA Contribution Limits Chart – Overview of 2022 and 2023 contribution limits, deductibility phase-out ranges for Traditional IRAs, and eligibility phase-out ranges for Roth IRAs

- Annual Contributions FAQs – Look through our commonly asked questions regarding contribution limits, eligibility, and the process to make a 2022 or 2023 contribution to your STRATA IRA.

- IRS Publication 590-A – Detailed explanations of all the IRA contribution rules, including a worksheet for calculating your eligible deduction amount if your MAGI falls in a phase-out range.

Automate Payments for Your 2023 Contributions

- ACH Contribution Authorization Agreement – Want to spread out your contribution deposits for 2023? You can set up recurring periodic deposits (e.g., monthly) for your IRA contributions.

Uninvested Cash in Your IRA?

Learn about alternative investment options with STRATA, or contact our self-directed IRA experts for more information.